Richemont: improved margins and profits

Sitthipong Pengjan/iStock Editorial via Getty Images

Swiss luxury company Compagnie Financière Richemont (OTCPK:CFRUY) is up 13% in trade as of this writing. The reason is no surprise. It has just published its half-year results. In my last report on CFRUY three weeks ago, I put a Hold rating on the stock based on two concerns. First, its operating margins were significantly lower than those of its peers. And second, China’s zero COVID-19 policy may continue to harm it for the foreseeable future. However, its latest figures allay both concerns, indicating that we can now expect better results for the company.

YNAP sale boosts margins

Despite strong revenue and net profit growth over the past fiscal year (FY22), Cartier owner Richemont lagged peers like LVMH (OTCPK:LVMUY) and Hermes (OTCPK:HESAY) in terms of operating margins. In this time of high inflation, luxury margins are particularly crucial to consider, as this is precisely what can make them relatively immune to the impact of rising prices. At 17.9%, its operating margin wasn’t bad, but with Hermès at 40% and LVMH at 26.7%, it wasn’t competitive either.

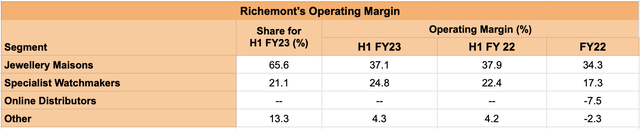

There was room for improvement, however, with the sale of a majority stake in online retailer Yoox Net-A-Porter. [YNAP] at London-based luxury fashion marketplace Farfetch (FTCH). Although exact figures for YNAP were not available, I had made rough estimates of the drag on its margins based on figures available for its online distributor segment. These indicated the possibility of an increase of about 4 percentage points in operating margin after the sale. In its latest update, Richemont wrote down its YNAP assets and presented information for continuing operations that reveals a bigger-than-expected jump in operating margin to 28.1% for the first half of the current fiscal year (April -September 2022, H1 FY23), with YNAP now represented as discontinued operations. This means that its margin no longer rivals that of Hermès in the luxury segment, and that it is even slightly higher than that of LVMH.

Source: Richemont Financial Company

There’s even more to love about its operating margin. It rose slightly from the 27.8% level seen in the comparative figures now available for the first half of FY22, as its Specialty Watchmakers and Others segments (which now include Fashion and Accessories, its watch components manufacturing division, Watchfinder and real estate businesses) fell slightly from its largest division, Jewelery Maisons (see chart above). Additionally, compared to FY22, its margins for all three segments have improved. Note that the Other segment is not fully comparable, since Watchfinder was part of online distributors before, which no longer exists as a category. Its move to Other likely contributed to the category’s positive operating margin in the last half of the year, although Richemont cites strong performances from other brands like leather goods brand Delvaux and casual sportswear brand Peter Millar.

Improved sales in Asia-Pacific

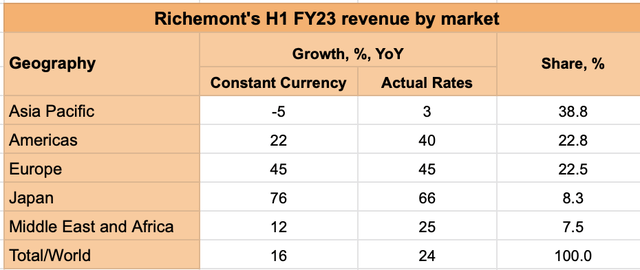

Richemont’s sales figures have also improved since its last update for Q1 FY23 (ending June 30, 2022). At the time, it reported a 20% year-over-year (YoY) revenue increase, which rose to 24% for the first half of FY23 on the back of a slight upward revision from its first quarter figures, but mainly due to improved performance in the second quarter as Asia-Pacific sales improved even though other segments showed a relative slowdown compared to their growth levels high in the first trimester. Revenue for his company in Asia Pacific actually rose 3% after a 16% drop in the second quarter. However, this is partly due to a positive currency effect. At constant currency, sales in the region were down another 5% but signs of renewed growth are present with Q2 growth of 6% at constant currency. The growth rate is not ideal but is still good news as the region is its largest market and the Chinese economy is expected to grow relatively rapidly next year even as major European and US economies slow down.

Source: Richemont Financial Company

Attractive valuations

Richemont’s latest results also provide insight into its earnings from continuing operations, which look promising. It reported a net loss after YNAP’s writedown, but since that’s likely the full amount, the numbers from the next update could be much better. Additionally, its earnings from continuing operations for the first half of FY22 are 11.2% higher than last year, indicating the extent of the slowdown in its YNAP operations. Even accounting for these higher earnings levels for last year, its earnings from continuing operations jumped 40% for the first half of FY23. The TTM earnings estimate from continuing operations based on the increase in H1 FY22 earnings after removing the impact of YNAP on H2 FY22 earnings, and its latest H1 FY23 earnings from continuing operations give a P/E of 20x, down from 28x before the update is entered.

This not only makes CFRUY more attractive compared to the previous one, but also makes it more competitive against peers like Hermes and LVMH, which have P/Es at 50.3x and 25.3x respectively. Both companies have seen much higher growth in net profits over the past year and also posted stronger margins, which partly explains this. Moreover, their long-term price performance is also better. Still, I think there could be a bit more upside for Richemont in the near term, from the fact that it’s still down almost 26% year-to-date, down from a 17% drop, 1% for the S&P 500 (SP500).

And then ?

However, a short-term rise does not yet translate into a medium-term buy. The next year could be difficult for it, as for most other companies, given the impending recession in the United States and Western Europe. Also, as winter progresses, we don’t know what will happen next when it comes to COVID-19. That said, its longer-term performance could still improve and valuations look more attractive now. I go from a Hold odds to a Buy on Richemont odds.